A Case for Commercial Equipment Leasing

LeaseWorld.org original produced by John Elliott of Jocova Financial

How Equipment Dealers Influence Customers Decisions for Equipment

Equipment dealers have a significant role in the underlying success of many businesses. They advise, service, and sell the equipment that drives both small and large businesses alike. They are relied on heavily to supply the right equipment that meets the needs of their customers and their job-related tasks. Dealers forge strong relationships based on trust with their customers for guidance about what equipment they should be operating for ease of use, longevity, and utility. They can also influence the purchase of any new products and services that are available. All this being said, the impact on business-owner customers could be quite substantial regarding how the customer performs in the market, the markets they go after, and how their services are delivered. Dealers can provide experiences and cases studies to customers with reference to equipment and what has been done for other businesses; further guiding the customers; decision-making process.

How Equipment Financing Decisions Impact Customer Success

Almost equally important as the equipment itself is the financial guidance and options the equipment dealer provides and has at their disposal to assist their customers. The dealer, therefore, needs to have a firm grasp of equipment financing options, how they work and can be applied to equipment purchases. Many dealers will have two main categories of financing options available. The first is a personal credit-based product and the second is a commercial financing or leasing product. If the client is a business (and for the sake of our discussion, it is), they should seldom consider a personal-loan-based product vs. commercial financing1. The driving factor in this is that businesses should be borrowing in their business-incorporated entity name. This ensures that credit checks and decisions are based on the commercial credit bureaus; with no ties back to the personal business owner. Exceptions to this would be when the business owner is a sole proprietor of a newly-incorporated business; and in these circumstances, commercial information would either be non-existent or lacking, and personal support would be required but still recommend for commercial financing or leasing products.

Which Financing Option is Best for Equipment Purchases

What happens when the message about what financing options to offer customers is murky and one process seems faster and easier than another? Which one is right? What is given up for one option over the other? What are the benefits? What are the negative aspects? What is best for the customer buying the equipment? This can lead to many barriers to the business owner getting the best financing options. Many dealers are set up with two main categories of finance offerings as noted above (personal and commercial), and some may try to direct customers to use their personal details to apply for a loan to acquire equipment, even if they are going to use the equipment for their business. The main reason for this is that personal loan portals at the dealer level provide nearly an instant credit decision often while the customer is in the showroom and wanting to purchase.

Equipment Leasing simplified. Check out Jocova Financial

The commercial process is marginally different. The customer’s credit application is gathered and submitted for processing but rarely is the decision instantaneous. Rather, the application is sent to the commercial financing company who processes the application; this process could take as little as an hour or up to one or two business days, depending on the transaction amount and the quality of the information presented on the application. This time barrier can sometimes be the difference between getting the right financing product and not finalizing a deal. Why? One reason is that immediate personal loans while the customers are still in the showroom are considered the path of least resistance. The customer is present and the dealer does not want to risk having them walk away from a sale or re-thinking their decision if they leave and wait while the transaction is being processed.

An example of this is in the landscape and property maintenance industry and in particular the spring-and summer-related equipment such as high-cost mowers and trailers that landscape companies purchase to use in their commercial ventures. These types of equipment dealers have options where there are both personal (consumer) and commercial financing options available.

Is Personal Lending Easier than Commercial Financing?

In short, personal loans for purchases at the equipment dealers is simple. It is done through a web portal and general information such as your name, address, date of birth and employment details are taken and then the computer does a quick check of your credit bureau and approvals or declines the transaction in real-time and then the consumer can leave straight away with the equipment.

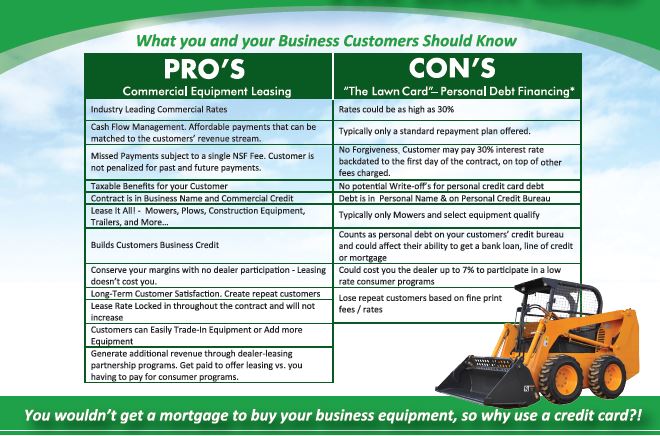

However, using personal debt can even have greater ramifications on one’s situation such as impacting your credit score, increasing your credit utilization and debt service, which may impact your ability to use your credit for other personal credit-related necessities such as obtaining or renewing a mortgage, applying for a line of credit or getting a car loan.

Why is Commercial Equipment Leasing a More Involved Process?

While commercial financing of equipment can be quick, it can also take hours to access because of the number of factors that come into play when processing an application. These range from the legal corporate name and commercial bureaus, trade activity, time in business, type of business, the shareholder details, industry, cost of equipment, type of equipment, and more. Each of these factors plays into the credit-decision process and often requires a combination of computer scoring and real people to work the application and have it set up in a way that is best suited for the business borrower.

Equipment Leasing as the Right Financing Tool

There are so many equipment leasing companies offering deals that it’s hard for you to decide which one is best for your needs. As a first step, you want to research each companies you are considering through the financing & leasing association (ELFA & CFLA) as well as the Better Business Bureau. Whichever kind of business you have, it’s essential that your equipment financing is matched to the needs and seasonality of your business.

Have the Best Equipment Financing Companies Bid on Your Equipment Financing Needs

Your equipment dealer should be knowledgeable about your business, your needs, and any financial limitations you may have. That is why it’s so important to keep your business and personal financial lives separate.

You wouldn’t tow your boat with a motorcycle; you would use a truck, and you wouldn’t use a raft to send shipping containers across the ocean. So why would you use personal financing debt to acquire equipment for your business?

As stated above, most equipment financing companies can take up to a day to approve an equipment lease for the purchase of equipment, and if you need that new tractor or trailer right away, you’re going to be tempted to go for a personal loan. Think about the ramifications – for one thing, this large purchase will probably have an impact on your personal credit score and you will miss out on all the benefits equipment leasing affords.

Leasing your equipment has many advantages to consider for your business:

- By leasing your equipment, you are retaining control of your working capital.

- Leasing offers a lower upfront cost and may have potential tax-deductible treatment. Discuss with your accountant.

- Your monthly payments won’t increase over the term, so you will have better control of your budget and cash flow.

- You don’t have to obtain a large loan to finance the equipment and taxes.

- Businesses are constantly working within budgetary constraints. By leasing equipment, it allows your business to purchase more equipment or better quality equipment then otherwise would be affordable if you were to pay cash.

- Some leasing companies will lease equipment to you if your credit rating isn’t perfect, while personal loans are generally reserved for good credit customers.

- When you lease equipment, you put the equipment to work for your business making you money that in turns makes the monthly lease payments.

Top 10 Reasons to Use Equipment Leasing for Your Next Equipment Purchase

Also, check out the Section 179 in the USA tax code to see how much of your profit you can retain by deducting the leasing costs as an operating expense and in Canada see Capital cost allowance classes for guidance.

- Exceptions apply. Customers should check with their accountant to ensure they are using the best financing options available whether personal or commercial.